The prosperity of a few years ago, such as it was — profits were terrific, wages not so much — depended on a huge bubble in housing...” -- Paul Krugman, NY Times, Dec. 22, 2008

'What an ideology is, is a conceptual framework with the way people deal with reality... Everyone has one. You have to - to exist, you need an ideology. The question is whether it is accurate or not."-- Alan Greenspan, former chairman of the Federal Reserve, from 1987 to 2006, at the Congressional House oversight and government reform committee on 23 October 2008

Who would think that housing speculation, aided by government subsidies and tax policies, would be one of the "financial weapons of mass destruction"?

Something so simple as ensuring that all people have an adequate place to live became a financial weapon, a means for some to get rich quick, for some to collect votes, and for some to collect consulting fees for spouting conventional wisdom.

There is no "magic bullet" financial formula to close the gap between the cost of adequate housing and the low incomes of many households. Housing is expensive. There is no such thing as cheap housing -- unless it is unfit and in declining unsafe neighbourhoods.

Given that housing is expensive, why pursue policies that make housing even more expensive - measures that inflate house values by encouraging speculation?

All warnings were ignored. The unfettered, free-market ideologues, the money-grubbers and

the ignorant in positions of power and influence went with the conventional wisdom of not only relying upon but also deregulating housing and related financial markets.

Encouraging homeownership is popular and profitable (for some). Advocates for directly helping low-income households were ignored. These "fuzzy thinking folks" favour the "inefficient" and "failed" method of providing housing subsidies directly to those in need rather than relying on market trickle down.

To save money Liberal Fiance Minister Paul Martin ended the social housing supply programs in 1993, a move the defeated Tories promised to do. His party promised to do the opposite. Since then, the neoliberal market ideology ruled in a knee-jerk fashion.

One Canadian example: In his September 30, 2002 column, “For rent: a tired out policy, no view, high price,” the Globe and Mail’s John Ibbitson complained that the federal government was about to spend some money on social housing. “Saints preserve us. The feds want to get back into public housing… the lessons of past failures forgotten.”

What is the answer for Canada? Follow the United States.

“So how should the state help these people? Build an apartment building, and charge them below-market rents? That may be best for a politician's ego, but not for the people in need.

“They need to find a way to buy a home, to start building equity and financial independence. They need tax credits or loan guarantees. One idea might be a federal program compelling banks to issue mortgages without down payments, amortized over 40 years, say, instead of 25, with Ottawa guaranteeing the mortgage in its early years.”

Fortunately, Canada did not follow the United States, though it did not provide much new social housing either.

Instead of trapping people in house payments they cannot afford in poor quality neighbourhoods in which people with options choose not to live, as in the United States, new social housing housing directly meets needs and helps build communities and neighbourhoods.

The crucial problem with social housing, which its opponents do not use in their policy arguments, is that it is non-market housing. No one can speculate with it or play financial games with it. It is simple. Build it and people live in it. Its purpose is to house people, not to be a financial investment -- other than as a long term societal investment in infrastructure, as good places to live for those who canot afford what the market has to offer.

The United States increased its homeownership rate temporarily by more than five percent, with Canadian government and private sector actors encouraging similar policies. It did so by turning every conceivable aspect of the house into a market commodity.

The New York Times is publishing a series of helpful analyses on the financial collapse. One conclusion is that during the Bush years all warning signs were ignored in order to push the deregulation let-the-market-alone ideology. In addition, the warnings about giving special tax breaks to homeowners, as Clinton did in 1997, proved to be correct.

Every step down the road to the financial collapse was taken in spite a clear warnings to the contrary. Canada only went part way down the road and may escape some of the worst outcomes.

(1) NY Times: White House Philosophy Stoked Mortgage Bonfire

"Eight years after arriving in Washington vowing to spread the dream of homeownership, Mr. Bush is leaving office, as he himself said recently, “faced with the prospect of a global meltdown” with roots in the housing sector he so ardently championed.... But the story of how we got here is partly one of Mr. Bush’s own making, according to a review of his tenure...

"Today, millions of Americans are facing foreclosure, homeownership rates are virtually no higher than when Mr. Bush took office, Fannie and Freddie are in a government conservatorship, and the bailout cost to taxpayers could run in the trillions." NY Times, December 20, 2008

In June 2002, President Bush unveiled a plan to increase the number of minority homeowners by 5.5 million. Instead of directly engaging in a prograam to assist lower income people his administration relied on market incentives and special mortgages, such as no money down and adjusable rate mortgages. This was during a period in which the incomes of most families remained relatively stagnant and house prices skyrocketed. We now know the outcome.

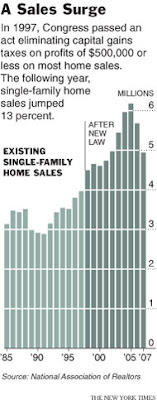

“Tonight, I propose a new tax cut for homeownership that says to every middle-income working family in this country, if you sell your home, you will not have to pay a capital gains tax on it ever — not ever.”

This was Bill Clinton at the 1996 Democratic Convention, making a campaign promise to counter a tax cut proposal of his opponent.

The housing tax break, exempting most home sales from capital gains taxes, was approved by Congress in 1997. It did not apply to other investments such as stocks or bonds, which were all taxed at rates of up to 20 percent.

This special tax treatment of the nation's housing stock exphasized the house as a investment vehicle. Again, we now know the outsome.

By itself, the change in the tax law did not cause the housing bubble, economist say. Several other factors — a relaxation of lending standards, a failure by regulators to intervene, a sharp decline in interest rates and a collective belief that house prices could never fall — probably played larger roles.But many economists say that the law had a noticeable impact, allowing home sales to become tax-free windfalls.

A recent study of the provision by an economist at the Federal Reserve suggests that the number of homes sold was almost 17 percent higher over the last decade than it would have been without the law.

Vernon L. Smith, a Nobel laureate and economics professor at George Mason University, has said the tax law change was responsible for “fueling the mother of all housing bubbles.”

By favoring real estate, the tax code pushed many Americans to begin thinking of their houses more as an investment than as a place to live. It helped change the national conversation about housing. Not only did real estate look like a can’t-miss investment for much of the last decade, it was also a tax-free one.

Together with the other housing subsidies that had already been in the tax code — the mortgage-interest deduction chief among them — the law gave people a motive to buy more and more real estate. Lax lending standar and low interest rates then gave people the means to do so. NY Times, December 18,2008